Over the past month, several reports highlight an amazing dichotomy in US energy production. A strong divergence exists between production trends in the oil and gas sector and the utility power generation sector. Each of these sectors has evolved in different directions, particularly when we consider the impact of these sectors on the economy and CO2 emissions.

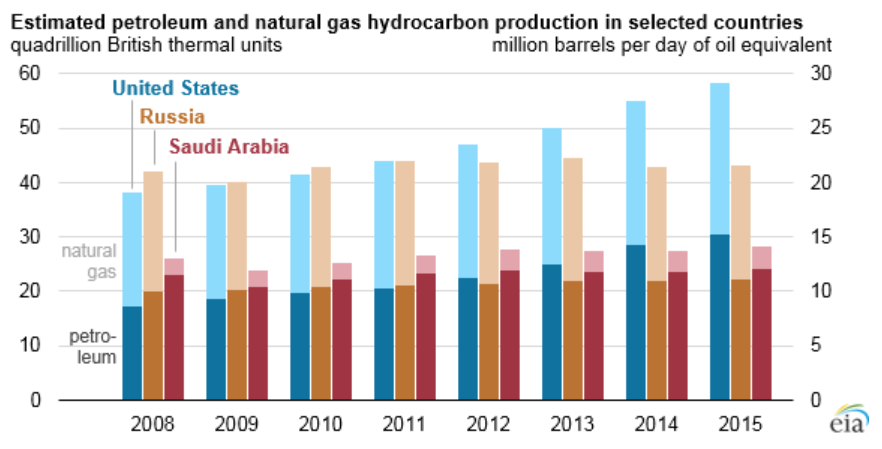

The first trend is that the US has become the world’s leading producer of petroleum and natural gas. The US surpassed Russia’s production in 2012 and Saudi Arabia’s the following year. Since 2011, US petroleum production has grown by approximately 1 million barrels per day each year. By 2015, this US dominance in oil production has expanded to the point where the US produces 20% more oil than Saudi Arabia and 35% more than Russia. Even in the face of falling prices in 2015, the US market position continued to expand.

Source: http://www.eia.gov/todayinenergy/detail.cfm?id=26352

A very divergent trend is seen in the utility power generation sector. Utilities are rapidly moving away from coal to lower or no emission CO2 sources. While that isn’t necessarily news, the magnitude of this trend and its recent impact on CO2 emissions may be surprising to many. CO2 emissions from the power plant sector have fallen to their lowest levels in 22 years. While we can argue about the strength of economic activity since the Great Recession, there is no doubt that a roughly 2% GDP growth rate should lead to higher CO2 emissions. Instead, in the face of this GDP growth, utility CO2 emissions declined by approximately 20% since 2008.

Source: http://www.eia.gov/todayinenergy/detail.cfm?id=26232

Natural gas, as a low cost fuel, has supplanted coal-based electricity across the country. But,renewable energy sources have also surged. In the first quarter of 2016, more renewable energy capacity was brought online than any other type of electricity generation. While renewables and natural gas are leading utility generation investments, coal-based plants continue to close across the country.

Perhaps oil and natural gas production will start to level out in 2016. Low prices, large declines in drilling rates, and slowly increasing electrification of the transportation sector haven’t fully run their course yet. In 2016, analysts expect an even stronger decline in utility-based CO2emissions as coal production continues to weaken as noted recently in this article: http://www.nytimes.com/2016/06/11/business/energy-environment/coal-production-decline.html

These large-scale trends show that, as a country, we can change our energy and emissions trajectory. We can bend the curve. The only question is when will we bend the curves in the same direction with a consistent, comprehensive energy policy?